User guide

Finding your way around the guide

To navigate between pages, click or tap the arrows to go forwards to the next page or backwards to the previous one. The arrows can be found either side of the page and at the bottom, too (circled in green, below).

Menu/table of contents

Click or tap on the three horizontal lines in the top-right of your screen to open the main menu/table of contents. This icon is always visible whether you're using a computer, tablet or smartphone. The menu will open on top of the page you’re on. Click on any section title to visit that section. Click the cross at any time to close the table of contents.

Text size

On a computer, you'll see three different sized letter 'A's in the top-right of your screen. On a smartphone or tablet these are visible when you open the menu (see above). If you’re having trouble reading the guide, click or tap on each of the different 'A's to change the size of the text to suit you.

Pictures

On some images you'll see a blue double-ended arrow icon. Clicking or tapping on this will expand the picture so you can see more detail. Click or tap on the blue cross to close the expanded image.

Where we think a group of images will be most useful to you, we've grouped them together in an image gallery. Simply use the blue left and right arrows to scroll through the carousel of pictures.

Links

If you see a word or phrase that's bold and dark blue, you can click or tap on it to find out more. The relevant website will open in a new tab.

Jargon

If you see a word or phrase underlined, click or tap on the word and small window will pop up with a short explanation. Close this pop-up by clicking or tapping the cross in the corner.

Help

On a computer, you'll see a question mark icon in the top-right of your screen. On a smartphone or tablet this is visible when you open the menu (see above).

Clicking or tapping on the question mark will open this user guide. It opens on top of the page you're on and you can close it any time by clicking or tapping the cross in the top-right corner.

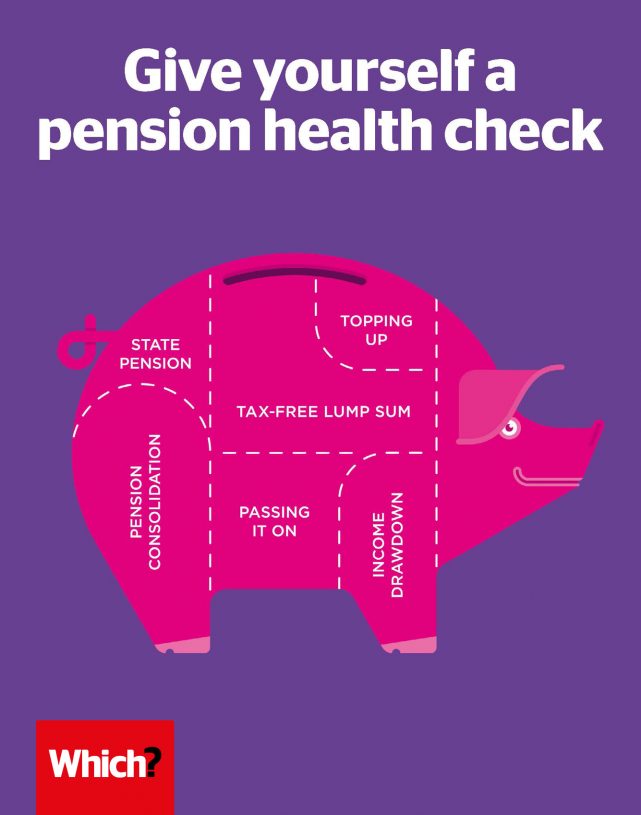

Getting the best deal from income drawdown

If you do opt for income drawdown in retirement, make sure you’ve explored all the options to get the arrangement that suits you the best.

Income drawdown is a flexible way to convert pension savings into income, and it doesn’t require you to buy an annuity. Recent surveys, including of our own Which? members, have found that a significant number of people are opting for the flexibility of a drawdown arrangement rather than buying an annuity. However, you should take financial advice before deciding what the right options are for you.

Q: Am I eligible for income drawdown?

A: With income drawdown, you keep your pension savings invested when you reach retirement and take money out of – or draw down from – your pension pot. You must be aged 55 or over and have a defined contribution pension to access your money in this way. You won’t normally be able to opt for income drawdown if you’re in a defined benefit scheme.

Q: How do I get an income drawdown plan?

A: Many providers now offer income drawdown products, each with different features and charges. You should shop around to find the offer best suited to your pension savings and take independent advice on the right provider for you.

Q: What are my options?

A: All new income drawdown arrangements set up after 6 April 2015 are known as ‘flexi-access drawdown’ plans. Under these plans, you can take up to 25% of your pension savings tax-free up front. There are no limits on how much you can withdraw from your remaining pension pot. You could withdraw it all in one go, set up regular monthly or annual payments, or take out lump sums as and when you need them.

Think carefully about your choices. Withdrawing all your money in one go could be useful if you need to repay a debt or make a big purchase, but it could leave you without sufficient income for the rest of your retirement. You may also have to pay extra tax if a large sum pushes you into a higher tax bracket for the year.

To see how long your pension pot might last if you opt for income drawdown, try our handy income drawdown calculator.

Similarly, if you’re making withdrawals, you’ll need to manage this carefully to be sure your cash will last. As a rough rule of thumb, you’ll need to be taking no more than 4% out of your fund each year to have a good chance of outliving your savings.

You may need to take professional advice on how to invest the money remaining in your pension pot. This is largely a question of your attitude to risk. Assets, such as stocks and shares, have, in the past at least, tended to deliver greater long-term returns. But they can also be volatile; your savings may fall as well as rise in value.

And bear in mind that income drawdown doesn’t have to be forever. You’ll still be able to buy an annuity later on.

Q: What do income drawdown plans cost?

A: Charges vary enormously from provider to provider – always seek expert advice on choosing the right plan for your circumstances. Research by Which? Money magazine has revealed a confusing array of charges levied by providers, including set-up charges, administration fees, management costs and plan levies. These eat into your pension fund, so it’s vital to factor them into your calculations.

Read more detailed information about your income drawdown options.

Q: What happens to my income drawdown plan when I die?

A: The amount of tax that will be due on your remaining pension after you die has been reduced. In the past it used to be a hefty 55%. These days, the tax liability now depends on the age at which you die:

- If you die under the age of 75, all your savings can be inherited tax-free - they can be taken as a regular income from your drawdown plan or as a single lump sum.

- If you die over the age of 75, your heirs will have to pay tax at their normal rate of income tax, whether they take your remaining fund as a lump sum or as a regular income.

The ease with which pension savings may be passed on to heirs is another reason why more people are now considering income drawdown pensions.

Q: Should I transfer out of a defined benefit scheme to access income drawdown?

A: Almost certainly not. While some advisers have argued the case for transferring money from defined benefit pension schemes to defined contribution alternatives in order to access drawdown products, the guaranteed benefits offered by the former mean this doesn’t make sense for the vast majority of people. The government insists that anyone considering making such a transfer should get independent financial advice if their pension fund is worth more than £30,000.