User guide

Finding your way around the guide

To navigate between pages, click or tap the arrows to go forwards to the next page or backwards to the previous one. The arrows can be found either side of the page and at the bottom, too (circled in green, below).

Menu/table of contents

Click or tap on the three horizontal lines in the top-right of your screen to open the main menu/table of contents. This icon is always visible whether you're using a computer, tablet or smartphone. The menu will open on top of the page you’re on. Click on any section title to visit that section. Click the cross at any time to close the table of contents.

Text size

On a computer, you'll see three different sized letter 'A's in the top-right of your screen. On a smartphone or tablet these are visible when you open the menu (see above). If you’re having trouble reading the guide, click or tap on each of the different 'A's to change the size of the text to suit you.

Pictures

On some images you'll see a blue double-ended arrow icon. Clicking or tapping on this will expand the picture so you can see more detail. Click or tap on the blue cross to close the expanded image.

Where we think a group of images will be most useful to you, we've grouped them together in an image gallery. Simply use the blue left and right arrows to scroll through the carousel of pictures.

Links

If you see a word or phrase that's bold and dark blue, you can click or tap on it to find out more. The relevant website will open in a new tab.

Jargon

If you see a word or phrase underlined, click or tap on the word and small window will pop up with a short explanation. Close this pop-up by clicking or tapping the cross in the corner.

Help

On a computer, you'll see a question mark icon in the top-right of your screen. On a smartphone or tablet this is visible when you open the menu (see above).

Clicking or tapping on the question mark will open this user guide. It opens on top of the page you're on and you can close it any time by clicking or tapping the cross in the top-right corner.

Where to get the best guidance

In an increasingly complex pensions landscape, getting reliable and relevant information will give you the best chance of making the right retirement-planning decisions.

Even people who feel confident about making financial decisions should seek guidance on how best to plan for retirement. There are so many options to consider that getting an expert perspective is crucial. Here are four potentially useful sources of information:

- Independent financial advisers (IFAs): IFAs can offer specialist advice at every stage of the process. They can help you choose a pension in the first place, advise on how your saving is progressing and talk to you about how to convert your fund into retirement income.

- Company pension advisers: Although they won’t be able to give you personalised financial advice, these advisers can provide important information about the options offered by your workplace scheme. Before you retire you should have access to someone within your organisation to answer questions about your workplace pension.

- Pension Wise: Pension Wise is a government-backed scheme that offers free and impartial pension guidance. Everyone over the age of 50 with a defined contribution pension is entitled to a free appointment, either in person or over the phone. The guidance is provided by Citizens Advice (in person) and The Pensions Advisory Service (by phone). Visit the Pension Wise website to book an appointment. See our tips below for how best to use the service.

- Which?: The Which? Money Helpline is part of your Which? membership and offers assistance with your financial affairs. The service provides one-to-one guidance on any personal finance matters over the telephone.

Making the best of Pension Wise

Get all your paperwork in place ahead of your Pension Wise consultation – everything covering your pension and your broader personal finances. Prepare to focus on the following questions. Then, following your appointment, you'll receive a printed summary of your options and the next steps to consider.

- When can I start drawing money from my pension?

- How can I take money from my pension?

- I want a guaranteed income. What are my options?

- I want flexibility. What are my options?

- I want a lump sum. What are my options?

- I want to take the whole lot in one go. What are my options?

- Could I run out of money?

- Should I consider a mix of different options?

- Do I pay tax on my pension? How much?

- Do I have to complete a tax return when I take my pension?

- What happens to my pension if I die?

- If I need further help, where should I go?

How do I choose an independent financial adviser (IFA)?

Details of authorised IFAs and how to contact them are available from groups such as the Personal Finance Society and the Financial Conduct Authority. Consider the following factors as you think about who to go for:

-

Your specific needs: If you need retirement advice, it might be best to go for an adviser who specialises in pensions. If you need a complete financial plan, go for an adviser who offers the whole package.

-

Qualifications: Legislation requires all advisers to be qualified to a certain level, but it’s worth checking that they are. Look out for extra qualifications, too, as that will show they’ve gone the extra mile.

-

Fees: Don’t take the fee the adviser quotes as gospel. If you think you should be paying less, discuss it with them. You may be offered different structures for fees – some charge a percentage of your assets; others use fixed fees. Learn more about how you will be charged for financial advice.

-

Personalisation: Be sure you’re not paying for generic advice that could apply to anyone; ask questions about the suitability of the recommended products for your situation.

-

Empathy: It’s important to feel you can forge a relationship with your adviser, as you will be trusting them with your financial wellbeing.

You may have very specific questions about your pensions, but, as you discuss your retirement planning with advisers, make sure you cover all the key topics.

1. When can I aim to retire?

Retirement is no longer a fixed time in your life – you can take early retirement or carry on working beyond state pension age. If you decide to retire early, you can start claiming your workplace or private pension from age 55, but your state pension won’t be available until you reach state pension age. You can also delay drawing your state pension. Ask advisers and providers for projections of your pensions at your chosen retirement date, plus guidance on what you need to do to hit your target level of income on time.

2. What help can I get from the state?

The state offers pension benefits in two different ways. First, you’re entitled to retirement benefits, such as the state pension, and it’s important to check how much you’re on target to receive. In addition, generous tax reliefs are available on contributions to private and workplace pensions, which increase the value of every penny you save in this way. Ask your advisers for guidance on how best to maximise tax efficiency.

3. Do I need to top up my pension income?

Once you’ve worked out how much money you’re getting and how much you'll need in retirement, you may find that you have a shortfall. But don’t panic – you can boost your income by making additional contributions, or you could choose to retire later.

4. Do I need to change my pension investments?

One reason your pension planning may be off target is that your investments aren’t working as you'd hoped. It may be that your investment strategy isn’t quite right – you are being too cautious, for example – or that you’ve got the right strategy, but the funds you’ve chosen are underperforming. Seek advice about whether it’s time to change course.

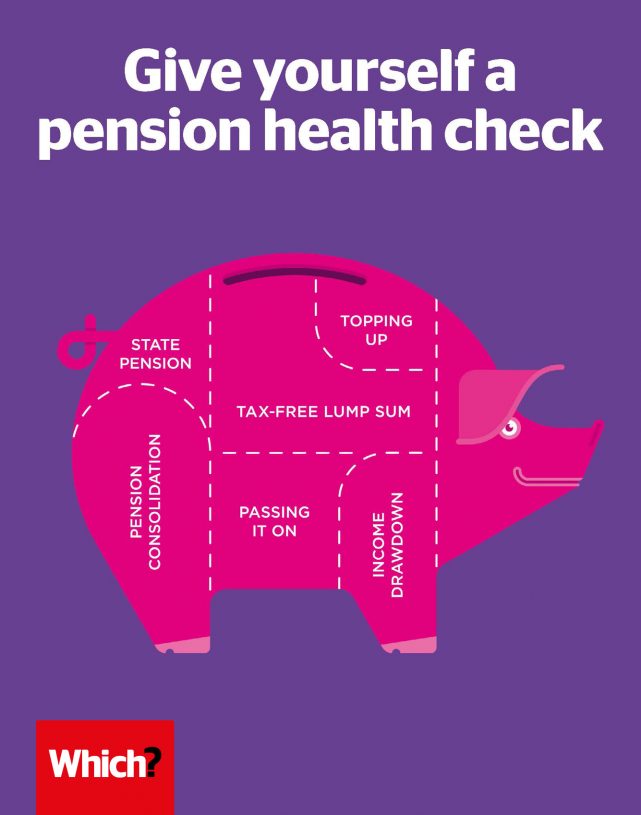

5. Should I consolidate my pots?

As you get nearer to retirement, you may decide you want to consolidate all your workplace and personal pensions in one place. This may be a good idea if you’re unhappy with your existing arrangements and you think your investments are underperforming. It also makes buying an annuity or going into drawdown easier, as all your money will be in one place. However, beware of exit penalties – you’ll have less time to recoup the cost before you retire.

6. Can I take a tax-free lump sum on retirement?

Before you take a lump sum, talk to advisers about the impact it will have on your pension pot – be careful because you’ll be left with less money with which to buy an annuity or to use for income drawdown.

7. Should I buy an annuity or take income drawdown?

Always take expert advice on how you want to take your pension income. If an annuity is the best option for you, an adviser can help you shop around for the best deal. If you’re going for income drawdown you'll need advice on how best to invest your savings, when and how much income you can withdraw, and how to structure your arrangements.